Conventional Loan Payment Calculator and Strategy Guide

When you're shopping for a home or preparing to apply for a

conventional loan, one question dominates every conversation: What

will my monthly payment be? This single number determines what you

can afford and how a potential home purchase fits into your overall

financial picture.

When you're shopping for a home or preparing to apply for a

conventional loan, one question dominates every conversation: What

will my monthly payment be? This single number determines what you

can afford and how a potential home purchase fits into your overall

financial picture.

However, that monthly payment figure is far more complex than it appears at first glance. It comprises several moving parts working together, and studying each component can reveal opportunities to save substantial amounts of money or accelerate your equity building.

This guide breaks down the components of a conventional loan payment, shows you how to use a payment calculator effectively, and explores proven ways to manage - or even reduce - what you pay over time.

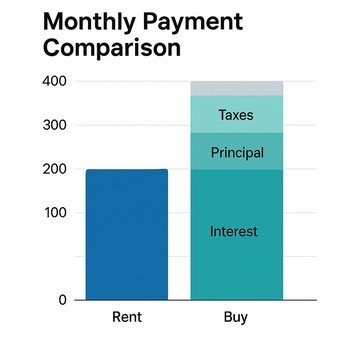

What Is Included in Your Monthly Payment?

Lenders use the acronym PITI to describe the core components of a standard mortgage payment. For most conventional loans, your monthly payment includes all four of these items, bundled into a single bill.

Principal: Paying Down What You Borrowed

The principal is the amount of money you actually borrowed to purchase the house. If you took out a $300,000 loan, the principal balance starts at $300,000. Each month, a portion of your payment goes toward reducing this amount.

In the early years of the loan, this principal portion is remarkably small - sometimes just a few hundred dollars. As you get closer to paying off the mortgage, the principal portion grows substantially larger, eventually comprising the majority of your monthly payment.

Interest: The Cost of Borrowing

Interest is the fee the lender charges you for the privilege of borrowing money. It is calculated as a percentage of your outstanding loan balance. In the beginning, when your balance is at its highest, the interest portion of your payment is also at its peak.

Over time, as you pay down the principal, the interest charged each month slowly decreases. This is why making extra principal payments early in your loan term can have such a dramatic impact on your entire interest paid over the life of the loan.

Taxes: The Local Government Share

Lenders typically collect property taxes as part of your monthly payment and hold the funds in an escrow account. When your property tax bill comes due, the lender pays it on your behalf from the escrow funds.

This arrangement guarantees the local government gets paid and protects the lender's investment from potential tax liens. Property tax rates differ greatly by location, making your home's address a major factor in your total monthly payment.

Insurance: Protecting the Asset

Just like with taxes, lenders require you to carry homeowners insurance and often collect the premium through your escrow account. This insurance protects the physical structure of your home and your personal belongings from damage due to fire, theft, and other covered events.

It also provides liability coverage if someone is injured on your property and holds you responsible. Depending on where you live, you may need additional coverage types:

-

Private Mortgage Insurance (PMI): Required on conventional loans if your down payment is less than 20%. It protects the lender if you default, not you directly. Once you reach 20% equity in your home, you can request that it be removed. Learn more about private mortgage insurance and how it affects your payment.

-

Flood Insurance: Required if your property is located in a designated high-risk flood zone according to FEMA maps.

-

Earthquake Insurance: May be required or strongly recommended in earthquake-prone areas, particularly in California and the Pacific Northwest.

Additional Fees

You may also have homeowners' association (HOA) fees included in your monthly payment if your lender manages them through escrow. Understanding all these components comprehensively is essential for precisely evaluating your overall affordability and long-term housing costs.

How to Use a Conventional Loan Payment Calculator

Using a monthly payment calculator is a simple and highly effective way to estimate your total housing costs before committing to a loan. You only need a few key inputs to get an accurate and realistic picture of your monthly obligations.

Key Inputs You Need

-

Loan Amount: The home's purchase price minus your down payment. Use our down payment calculator to see how different down payment levels affect your total loan amount and monthly payment.

-

Interest Rate: The current rate you expect to be charged on the loan. Shop around with multiple lenders, as rates can fluctuate markedly based on your credit score and market conditions.

-

Loan Term: The length of your loan, typically 15 or 30 years. Each term offers different advantages in monthly payments and total interest charged.

-

Property Taxes: Look up the annual tax rate for the particular area where you are buying. Divide by 12 to estimate your monthly property tax portion.

-

Homeowners Insurance: Get a detailed quote from an insurance agent for the specific property and coverage levels you need.

-

PMI Estimate: If your down payment is under 20%, factor in an extra 0.5% of the loan amount divided by 12 to estimate your monthly PMI cost.

Reading the Results

A quality calculator will show you a complete breakdown, not just a single bottom-line number. You will see exactly how much of each monthly payment goes toward principal, interest, taxes, insurance, and PMI. This in-depth breakdown helps you understand where your money is going each month.

For example, if the taxes seem high, you might look for a home in a different area with lower property tax rates. If PMI is costly, you might decide to save for a larger down payment to avoid PMI altogether.

Why a Payment Calculator Is a Smart Tool

A mortgage calculator is far more than just a number cruncher or financial curiosity. It is a tactical planning tool that helps you make genuinely well-informed decisions before you ever speak with a lender or commit to a home purchase.

-

Determine Affordability: Test different home prices and interest rates to find a comfortable budget that matches your income and expenses.

-

Compare Loan Terms: See the trade-off between a 15-year and 30-year loan in terms of monthly payments and total interest accrued over the life of the loan.

-

Assess Down Payment Impact: Visualize how a larger down payment lowers your monthly payment and may eliminate PMI costs.

Using a calculator provides a strong, data-backed starting point, allowing you to approach the homebuying process with certainty and clarity about your financial capacity.

Comparing Loan Terms: 15-Year vs. 30-Year

The loan term you choose has a massive impact on your monthly payment and your long-term costs. The 30-year loan is the most common because it offers a lower monthly payment, making homeownership accessible to more buyers.

However, a 15-year loan builds equity faster and saves significantly on interest over the life of the loan. Choosing between them depends on your cash flow circumstances and long-term financial goals.

| Loan Term | Monthly Payment (Estimate) | Aggregate Interest Paid (Estimate) | Best For |

|---|---|---|---|

| 30-Year Fixed | Lower | Higher | Buyers who need lower monthly payments for budget flexibility. |

| 15-Year Fixed | Higher | Much Lower | Buyers who can afford higher payments and want to build wealth faster. |

If you can handle the higher monthly payment, a 15-year term builds wealth faster and saves you tens of thousands in interest. If you need breathing room in your monthly budget, a 30-year term keeps your costs lower and provides financial adaptability.

Mortgage Payment Strategies

Beyond the standard monthly payment, there are alternative strategies that can help you save on interest and build equity faster. These methods can turn your mortgage into a powerful wealth-building tool rather than simply a monthly obligation.

The Bi-Weekly Mortgage Payment Strategy

A bi-weekly mortgage payment involves making half of your monthly payment every two weeks instead of paying once per month. This simple but elegant change creates a powerful acceleration effect that can save you tens of thousands of dollars in interest and shorten your loan term by years.

How It Works: The 26-Payment Magic

Because there are 52 weeks in a year, making payments every two weeks results in 26 half-payments per year. This is mathematically equivalent to making 13 full monthly payments per year instead of the standard 12 payments.

Example: If your monthly payment is $2,000:

- Monthly Plan: 12 payments × $2,000 = $24,000 per year

- Bi-Weekly Plan: 26 payments × $1,000 = $26,000 per year

- Extra Payment: $2,000 (one full payment) goes directly toward your principal each year

The Impact on Your Loan

The extra annual principal payment creates a snowball effect, reducing your loan balance faster and substantially cutting the total interest you will pay. This acceleration increases over time, creating substantial savings.

For a $300,000 mortgage at 6.5% interest:

- Monthly Plan: Paid off in 30 years, with $382,633 in total interest

- Bi-Weekly Plan: Paid off in 25 years and 2 months, with $284,803 in total interest

- Savings: $97,830 in interest and nearly 5 years off your loan term

For a $500,000 mortgage at 7% interest:

- Monthly Plan: 30 years, $698,757 in total interest

- Bi-Weekly Plan: 24 years, 8 months, $517,392 in total interest

- Savings: $181,365 in interest and over 5 years off your loan term

Pros and Cons of Bi-Weekly Payments

| Advantages | Disadvantages & Considerations |

|---|---|

| Significant Interest Savings: The primary benefit is the huge reduction in total interest. | Cash Flow Impact: You must budget for the equivalent of 13 payments a year. |

| Faster Equity Building: You own more of your home sooner. | Less Liquidity: Extra money is tied up in your home and cannot be easily accessed. |

| Forced Savings: It creates a disciplined, automatic savings habit. | Opportunity Cost: The extra money could potentially earn a higher return if invested elsewhere. |

| Psychological Benefits: Being mortgage-free years earlier is a major relief. | Lender Fees: Formal bi-weekly programs may come with setup and transaction fees. |

How to Implement the Strategy

You do not necessarily need a formal program or service to achieve bi-weekly payment benefits. You can achieve the same result with a simple "Do-It-Yourself" (DIY) approach that requires no special agreements or fees.

-

Method 1: Add 1/12 of your monthly payment to each monthly payment (e.g., pay $2,166.67 instead of $2,000).

-

Method 2: Make one extra full monthly payment directly to your principal each year, either in one lump sum or spread across several months.

This strategy works best for homeowners with stable incomes, a long-term outlook on their property, and a sincere desire for a guaranteed, low-risk return on their money.

Making Extra Principal Payments

You do not need a formal plan or special program to pay off your mortgage early and save on interest. Any time you send in extra money and explicitly designate it for "principal reduction," you immediately shorten your loan term.

Small amounts add up remarkably quickly: Even an extra $50 or $100 per month makes an important difference over 30 years, possibly saving thousands in interest. One-time payments such as tax refunds, work bonuses, inheritance money, or gifts can be applied directly to the principal for maximum impact.

Check with your lender to ensure there is no prepayment penalty on your specific loan (most conventional loans do not have them) and confirm that your extra payments are being applied to the principal correctly each month.

The Interest-Only Mortgage Payment Strategy

An interest-only mortgage allows you to pay only the interest charges for a set period, typically 5 to 10 years. During this time, your monthly payments are lower, but your principal balance does not decrease, meaning you build no equity through your payments.

This is a less common strategy that carries major risks and is generally suited only for specific financial situations. It calls for rigorous planning and a clear understanding of the implications.

How It Works: The Two-Phase Structure

Phase 1: Interest-Only Period (Years 1-10)

- You pay only the interest on the loan balance

- Monthly payments are at their lowest point in the life of the loan

- The loan balance remains completely unchanged (no equity is built through payments)

Phase 2: Amortization Period (Years 11-30)

- You must pay both principal and interest on the remaining balance

- Monthly payments increase considerably to amortize the remaining balance over the shortened term fully

Payment Calculation Example

Loan: $500,000 at 6.5% interest on a 30-year term

- Interest-Only Period (Years 1-10): Monthly payment = $2,708 (interest only)

- Amortization Period (Years 11-30): Monthly payment = $3,789 (principal + interest)

- Payment Shock: A 40% increase ($1,081 more per month)

Pros and Cons of Interest-Only Payments

| Advantages | Disadvantages & Considerations |

|---|---|

| Lower Initial Payments: Frees up significant cash flow for other purposes. | Significant Payment Shock: Monthly costs can skyrocket once the interest-only period ends. |

| Investment Leverage: The saved cash can be invested for a higher potential return. | No Equity Building: You build no equity through payments; you rely solely on appreciation. |

| Tactical Agility: Useful for those expecting a future income increase. | Market Risk: If property values fall, you could owe more than your home is worth. |

| Tax Advantages: All payments are tax-deductible interest (subject to IRS limits). | Refinancing Pressure: You may be forced to refinance at an unfavorable time. |

When Does an Interest-Only Mortgage Make Sense?

This is a sophisticated financial instrument best suited for specific situations and borrower profiles. Interest-only mortgages are not appropriate for everyone and call for thorough consideration.

-

High-Income Professionals: Those with predictable, significant income growth on the horizon and substantial savings.

-

Real Estate Investors: Those who want to maximize cash flow from a rental property to fund other investments or property acquisitions.

-

Borrowers with a Clear Investment Plan: Those who have a solid, vetted strategy to earn a return on the saved money that exceeds their mortgage rate.

-

Short-Term Owners: Those who plan to sell the property before the interest-only period ends and refinance into a standard loan.

Interest-only mortgages carry major risks and are not suitable for most first-time homebuyers. They require a high credit score, a substantial down payment, and a clear understanding of the potential payment shock when the interest-only period ends.

Making Smart Choices for Your Mortgage Future

Understanding your conventional loan options - from standard monthly payments to biweekly acceleration or interest-only structures - is absolutely key for your long-term financial well-being and wealth-building. Each strategy carries different benefits and risks that accord with specific financial situations, income levels, and goals.

The key to successful mortgage management is matching your payment strategy to your financial capacity, risk tolerance, and long-range objectives. Employ tools like our monthly payment calculator to model different scenarios and see real numbers. Through thoroughly understanding your options and their consequences, you can optimize your mortgage for both near-term affordability and long-term wealth building.

Frequently Asked Questions

Can bi-weekly payments really save five years?

Yes, biweekly payments can save approximately 5 years on a standard 30-year mortgage by making an extra full payment each year. The cumulative effect of this extra payment goes directly to the principal, accelerating payoff and considerably reducing total interest paid over the life of the loan.

What is the difference between PMI and homeowners' insurance?

PMI (Private Mortgage Insurance) protects the lender if you default on your loan and is required when your down payment is under 20%. Homeowners insurance protects your property and belongings from damage and is required by all lenders regardless of down payment amount.

Should I choose a 15-year or 30-year mortgage?

Choose a 15-year mortgage if you can afford the higher monthly payment and want to build equity faster and save on interest. Choose a 30-year mortgage if you need lower monthly payments for budget flexibility and want more breathing room in your monthly cash flow.

Are interest-only mortgages a good investment strategy?

Interest-only mortgages are sophisticated tools suited only for high-income borrowers with clear investment plans and significant savings. They carry major risks, including payment shock, and are generally not appropriate for first-time homebuyers or those without strong financial positions.

What happens if I make extra principal payments?

Extra principal payments directly reduce your loan balance, accelerate equity building, and significantly reduce total interest paid. You can make extra payments without penalty on most conventional loans, though you should verify your specific loan terms with your lender.

Connect With Us

Please share – it really helps